Are you curious about what the qualified business income deduction (QBI) is and whether or not you can take advantage of it? If so, this article will provide an in-depth overview of the QBI deduction and answer the fundamental question: “Can I claim it?”

Given its complicated nature, understanding how to maximize your tax deductions on business income with the QBI deduction should be a top priority for anyone who is self-employed.

Learn all about it here, from what qualifies as eligible business income to when you can use this deduction and more. Let’s dive in!

What is the Qualified Business Income Deduction?

The Qualified Business Income Deduction (QBI) is a recently established tax deduction allowing businesses to deduct as much as 20% of their earnings. This deduction applies to sole proprietorships, partnerships, S corporations, certain trusts, and estates.

The QBI was introduced under the Tax Cuts and Jobs Act of 2017, which sought to provide tax relief for businesses and individuals by reducing income taxes and introducing other incentives.

The QBI has helped to promote business investment and stimulate economic growth throughout the United States.

How Does it Work?

The Qualified Business Income Deduction (QBI) is a great benefit for small business owners, providing the opportunity to deduct up to 20% of their earnings.

This deduction can be used to reduce your taxable income and thus lower your overall tax liability. Here’s a breakdown of exactly how the QBI works:

- Eligibility: The QBI applies to sole proprietorships, partnerships, S corporations, certain trusts, and estates.

- Income Limits: The deduction is limited to businesses with taxable income under $170,050 for single filers or $340,100 for joint filers.

- Types of Income: The QBI applies to business income from activities such as trade or business activities in which individuals are not materially participating.

- Amounts Deducted: Businesses are able to deduct up to 20% of their earnings, with certain exceptions such as certain publicly traded partnerships.

Which Business Types Can Claim the QBI Deduction?

The QBI deduction is for any specified service trade or business (SSTB) with taxable income under the specified limits. Let’s take a look at the business types that can claim this deduction:

Sole Proprietorships

A sole proprietorship is a business owned and operated by one individual. This type of business does not require registration and can be established in most states with little to no paperwork.

Partnerships

Partnerships are businesses owned by two or more individuals. This type of business is generally easier to set up and manage than a corporation.

S Corporations

An S Corporation is a type of business entity that offers limited liability protection to its owners, as well as certain tax benefits.

Certain Trusts and Estates

A trust is an entity that controls and manages assets for the benefit of a third party. An estate is the legal entity created when an individual dies, which includes their assets and liabilities.

| Business Entity | Can they claim QBI Deduction? | Notes |

|---|---|---|

| Sole Proprietorship | Yes | The deduction is claimed on the individual owner’s tax return. |

| Partnership | Yes | Each partner can claim their share of the QBI deduction on their individual tax returns. |

| S Corporation | Yes | The shareholders can claim their share of the QBI deduction on their individual tax returns. |

| Certain Trusts and Estates | Yes | QBI deductions can be taken on the trust or estate’s return if the income is retained, or on the beneficiary’s return if the income is distributed. |

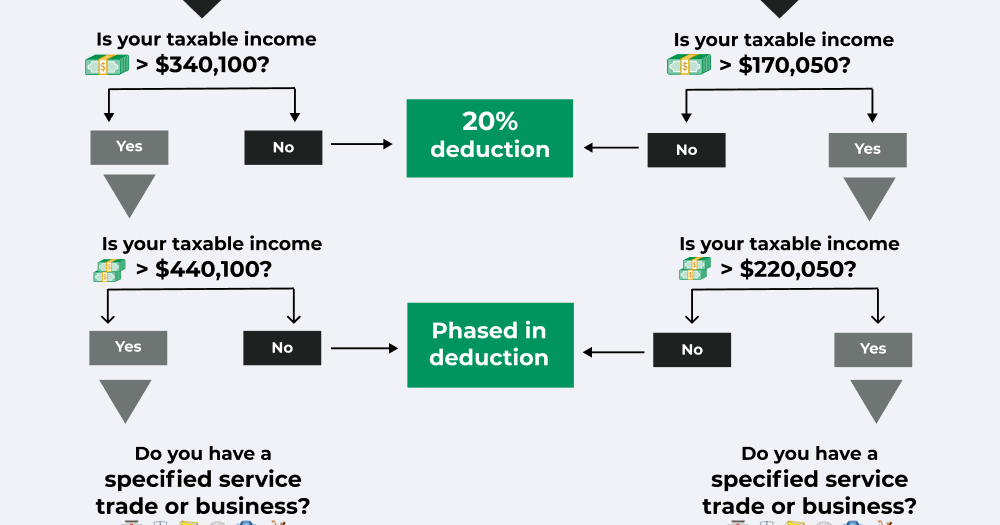

Tax Limits and Taxable Income

Your personal tax return determines whether you’re eligible for the QBI deduction, as well as how much of it you can claim.

The tax limits and taxable income limits vary based on filing status and other factors. Here are two tables on taxable income limits for 2022 and 2023:

| Filing status | Overall Taxable Income Limitation | Available deduction |

|---|---|---|

| Single | Less than $170,050 | 20% |

| Single | $170,050 to 220,050 | Partial deduction for SSTBs |

| Single | More than $220,050 | No deduction for SSTBs |

| Married Filing Jointly | Less than $340,100 | 20% deduction |

| Married Filing Jointly | $340,100 to $440,100 | Partial deduction for SSTBs |

| Married Filing Jointly | More than $440,100 | No deduction for SSTBs |

| Filing status | Overall Taxable Income Limitation | Available deduction |

|---|---|---|

| Single | Less than $182,100 | 20% |

| Single | $182,100 to 232,100 | Partial deduction for SSTBs |

| Single | More than $232,100 | No deduction for SSTBs |

| Married Filing Jointly | Less than $364,200 | 20% deduction |

| Married Filing Jointly | $364,200 to $464,200 | Partial deduction for SSTBs |

| Married Filing Jointly | More than $464,200 | No deduction for SSTBs |

What is Not Included in Qualified Business Income?

Qualified Business Income is a valuable deduction that may reduce the amount of taxes owed when filing.

However, there are certain items and types of income which may not qualify for this deduction. These include:

- Income from passive activities – Passive activities refer to those where the taxpayer does not materially participate in the business such as rental income or investments.

- Non-trade or non-business related income – This includes items such as interest or dividend income, capital gains, alimony received, certain gambling winnings, and other non-business related sources.

- Reasonable compensation – Reasonable compensation from an S Corporation is excluded from QBI, but allocated expenses such as health insurance and retirement contributions can be deducted from QBI to offset tax liability.

- Guaranteed payments for services rendered – If a partner provides services to a partnership or LLC, any guaranteed payments they receive are considered to be W-2 income and do not qualify for the QBI deduction.

- Capital gains – Capital gains are profits made on the sale of investments such as stocks and bonds. These profits also do not qualify for the QBI deduction.

Limitations of the QBI Deduction

The QBI deduction may offer considerable tax savings to businesses, but there are certain limitations that can restrict the amount of savings realized through this deduction. Below are a few of the major limitations:

Wage limitation

Higher earners, meaning those with incomes over $170,050 for single individuals or $340,100 for married filing jointly, may be subject to wage limitation restrictions which can reduce or eliminate QBI deduction eligibility.

20% cap

Generally speaking, the QBI deduction does not exceed 20% of qualified business income. While this is generally beneficial for businesses and self-employed individuals, it also means there’s a limit to the amount that can be deducted from taxable income.

Be sure to research how to file self-employment taxes as well as the best tax software for self-employed to make sure you’re paying your correct self-employment tax. Your state might not have one.

Aggregation requirements

The IRS requires certain trades or businesses to combine their incomes when taking advantage of the QBI deduction in an effort to prevent overstating deductions.

This includes multiple entities owned by one joint return filer as well as a partnership and S corporation owned by the same individual.

Employment rules

Employers offering employee benefits such as health insurance and retirement plans may have more complex rules around who qualifies for deductible wages as they relate to the QBI deduction.

Understanding these rules is vital in order to make sure eligible employees are given access to these benefits while staying compliant with IRS regulations.

How is the QBI Deduction Calculated?

Determine net income

The first step is to calculate the net income of the business by subtracting allowable deductions from gross income. This includes costs such as labor, cost of goods sold, and any other expenses related to running the business. Make sure to learn about the standard deduction 2022.

Subtract for depreciation, amortization, and depletion

Once net income has been determined, specific items such as depreciation and amortization need to be subtracted from this amount in order to arrive at a new figure referred to as “Qualified Business Income.”

Calculate taxable income without QBI deduction

To get total taxable income without taking advantage of the QBI deduction, subtract QBI from net income, then determine taxable income using normal methods.

Calculate taxable income with QBI deduction

To calculate taxable income with the QBI deduction applied, simply subtract 20% of qualified business income from total taxable income before adding on taxes owed on other forms of non-business related incomes such as capital gains or alimony received.

How to Claim the Qualified Business Income Deduction

Claiming the Qualified Business Income (QBI) deduction is a great way to reduce taxes owed on business income, but it’s important to understand how to structure the deductions properly in order to take full advantage of them. Here’s a step-by-step guide for claiming the QBI deduction:

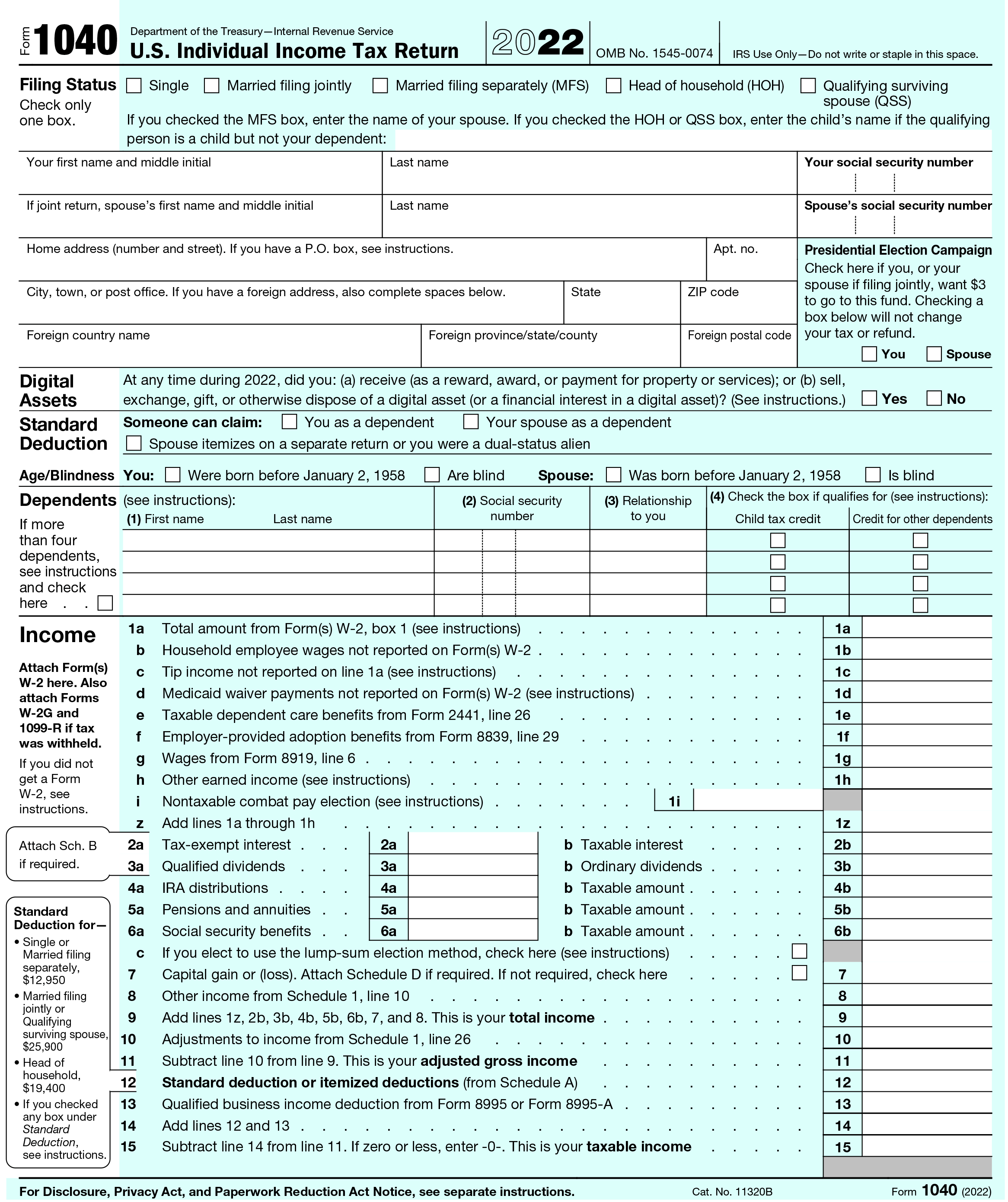

Step 1. Fill out Form 1040

The most basic form which needs to be filled out is Form 1040

. This will help determine your base taxable income before taking the QBI deduction into consideration. Make sure to declare all other types of income in addition to business income, such as capital gains or alimony received.

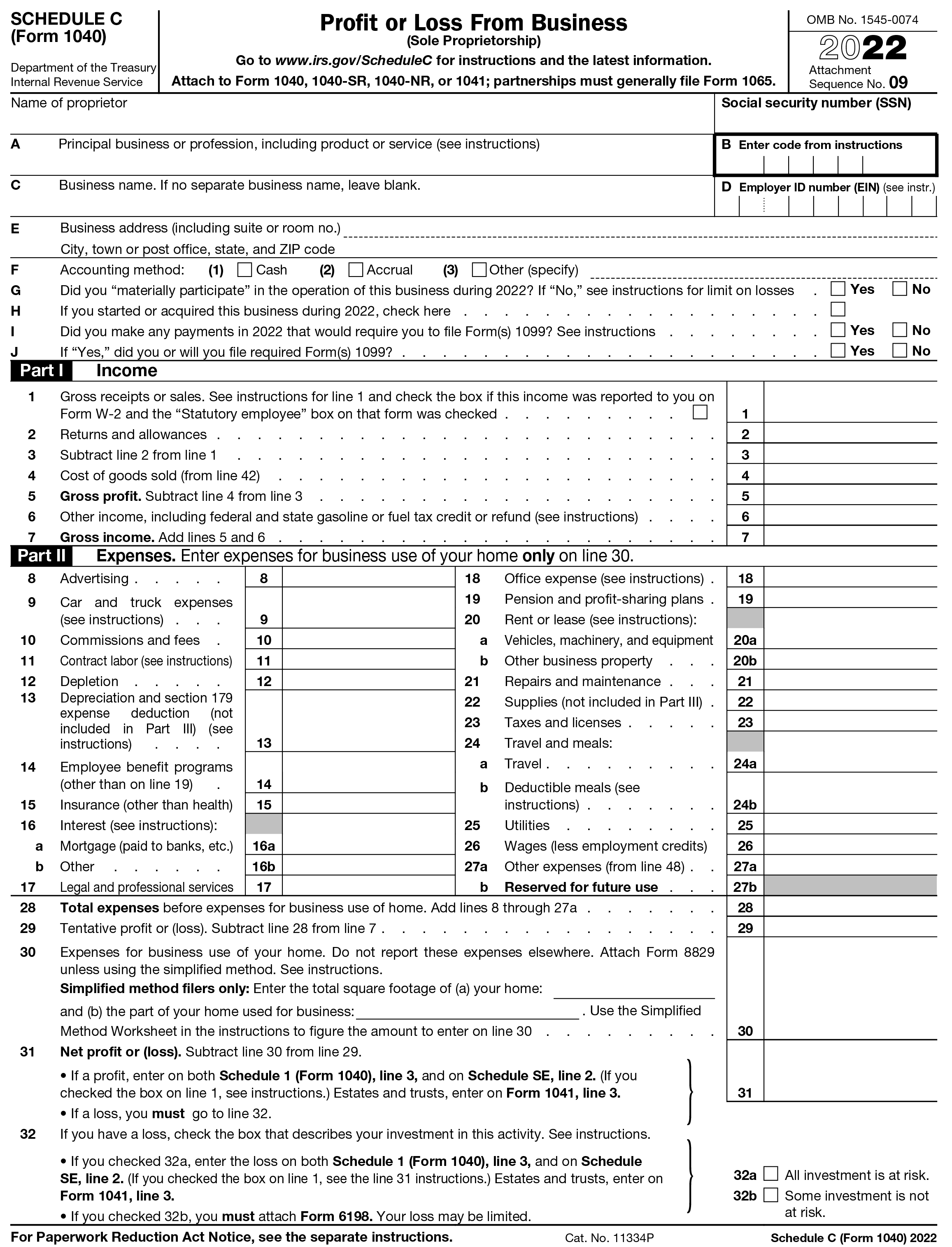

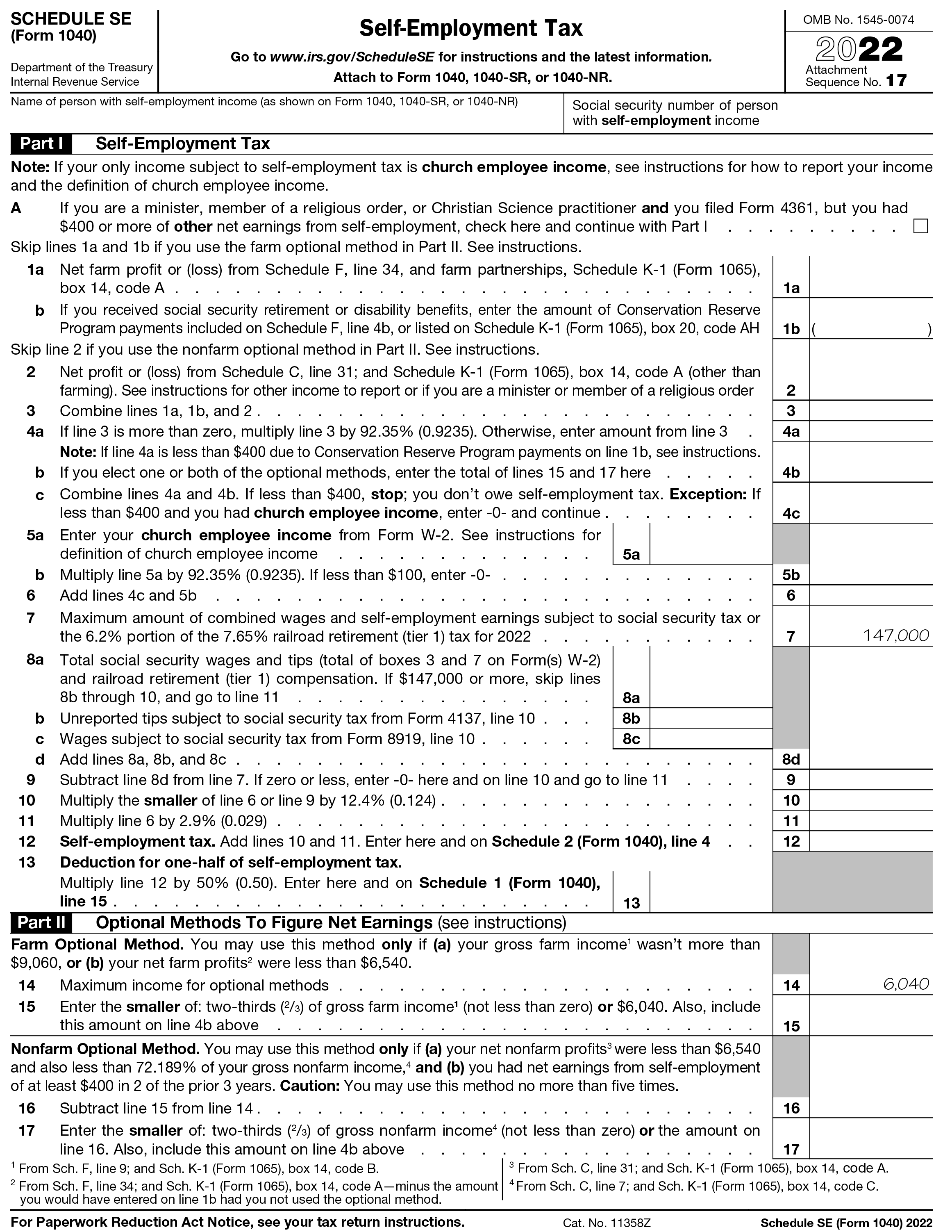

Step 2. Fill out Schedules C & SE

Depending on the type of business you own, you may need to fill out additional forms such as Schedules C and SE which detail your income from self-employment and any related expenses. Schedule C

is used to report income from an unincorporated business, while Schedule SE

is used for self-employment earnings. Make sure nondeductible expenses such as home office expenses aren’t included on these forms.

Step 3. Calculate net income

Once all relevant forms have been filled out, total net income can be calculated by subtracting allowable deductions from gross income on Schedule C or SE. You’ll want to make sure you include all relevant deductions, such as labor costs and cost of goods sold.

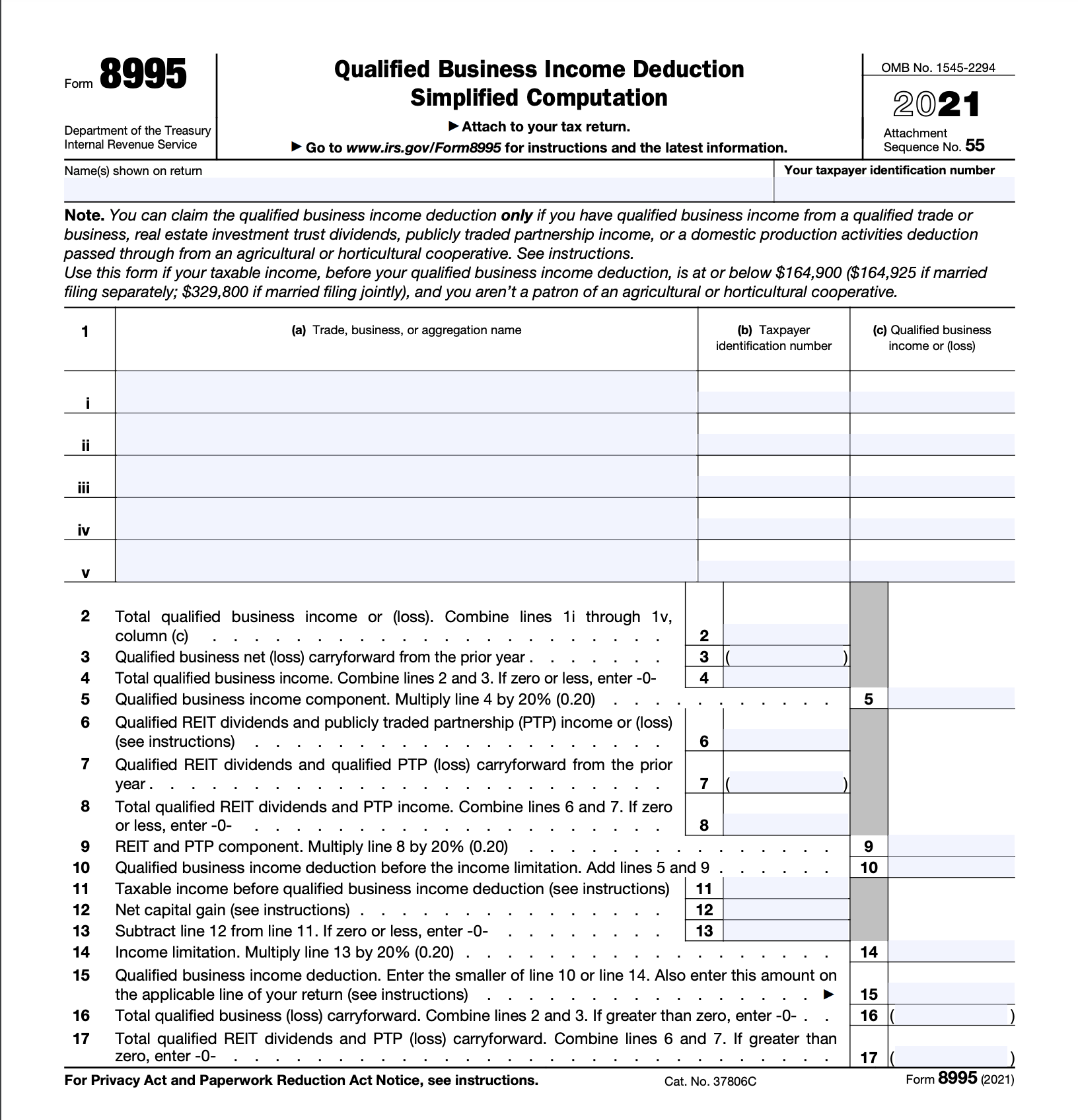

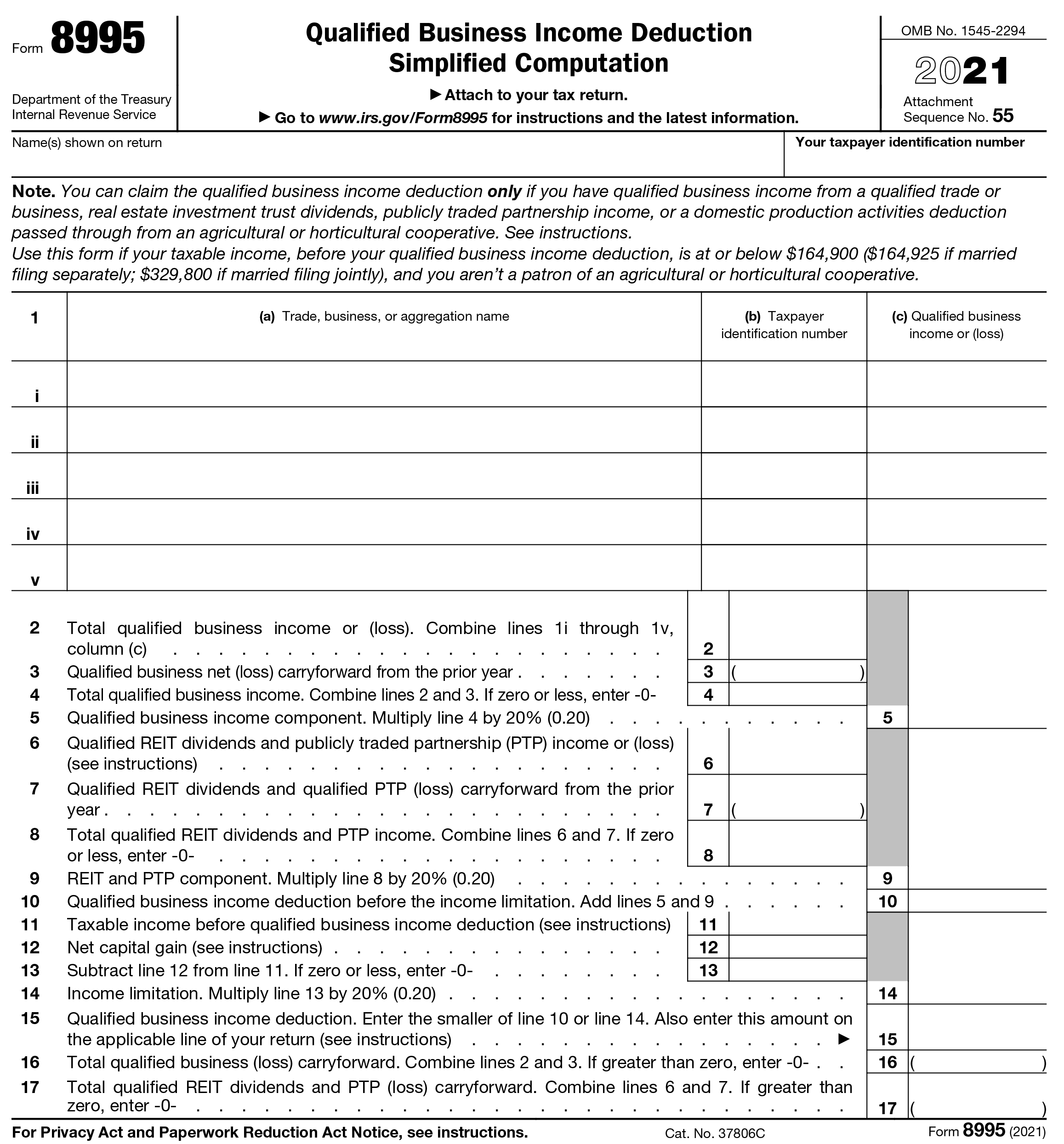

Step 4. Complete Form 8995

Details qualified business income and will help calculate eligibility for the QBI deduction and how much can be deducted. To fill out the form, you’ll need to enter total net income from Step 3, as well as any special deductions such as depreciation, amortization, or depletion.

Step 5. File tax return

Finally, after all of the required forms are completed, file your tax return and submit copies of Form 8995 along with your return in order to claim the QBI deduction. To ensure your deductions are accurate and compliant with IRS regulations, it’s a good idea to consult a qualified tax professional to learn how to file taxes properly for your specific needs.

QBI Deduction Example

Let’s look at a concrete example of how the qualified business income deduction (QBI) works in practice. Imagine a married filing jointly couple who earned $200,000 in taxable income from their business. Assuming all other criteria are met, they will be eligible for the QBI deduction and can deduct up to 20% of their earnings, or $40,000. This means the couple would only end up paying taxes on the remaining $160,000.

The Bottom Line

The qualified business income deduction is a complex tax break that has the potential to save you a lot of money, but it comes with a lot of rules and restrictions.

This article has provided an overview of the QBI deduction and some of the key considerations you need to take into account when determining if you’re eligible.

By doing your research and staying up to date on tax laws, you can make sure that you are taking full advantage of this valuable deduction. When in doubt, consult with a tax professional or follow the free tax advice the IRS provides on its website.

What does the QBI deduction reduce?

The qualified business income deduction (QBI) reduces taxable income and can help lower the overall amount you have to pay in taxes. By reducing your taxable income, the QBI deduction can effectively reduce your tax liability.

Can you claim qualified business income deductions on your rental property?

Yes, it is possible to claim the qualified business income deduction (QBI) on rental properties if they meet certain criteria.

To qualify for the QBI deduction, the property must be used in a trade or business and generate income. The rental activity must also be performed with some regularity and consistency, meaning that it is not just an occasional or incidental activity.

Finally, you must be actively involved in managing the rental property in order to be eligible for the deduction.

Is interest income included in the qualified business income tax deduction?

No, interest income is not eligible for the qualified business income deduction (QBI). The QBI deduction is intended to reduce the taxable income of businesses that meet certain criteria, such as being engaged in a trade or business with regularity and consistency and actively managed by the taxpayer.

Interest income, however, does not qualify as business income under this criteria and cannot be included in the QBI deduction.

Who Cannot take the QBI deduction?

Generally, anyone who meets the criteria outlined above can take the QBI. This includes individuals, trusts, and estates as well as pass-through businesses such as partnerships and LLCs.

However, there are certain taxpayers who are not eligible to receive the QBI deduction. These include specified service trades or businesses (SSTBs), qualified joint ventures, C corporations, certain single-member LLCs, and taxpayers excluded from claiming this deduction under the foreign or possession of income provisions.

Who qualifies for the 20% pass-through deduction?

In order to qualify for the 20% pass-through deduction, you must meet several criteria, including the following:

- Business Structure: Only entities structured as a sole proprietorship, partnership, S corporation, or an LLC treated as a sole proprietorship or partnership for tax purposes qualify. C corporations do not qualify for the deduction.

- Qualified Business Income: To qualify, the income must be from a U.S. trade or business. Qualified business income includes the net amount of income, gain, deduction, and loss from any qualified trade or business. Importantly, it doesn’t include investment-related income, wages, or reasonable compensation received by shareholders of S corporations or partners in a partnership.

- Taxpayer’s Taxable Income: The taxpayer’s taxable income must not exceed certain thresholds, which for the tax year 2021, is $164,900 for single filers and $329,800 for joint filers. If taxable income is above these thresholds, the amount of the QBI deduction may be limited or phased out. These thresholds are adjusted annually for inflation.

- Type of Business: For taxpayers with income above the threshold, the deduction may be limited or not available at all if the business is a specified service trade or business (SSTB). SSTBs include businesses in the fields of law, health, consulting, athletics, financial services, and any business where the principal asset is the reputation or skill of one or more of its employees or owners.

- W-2 Wages and Capital Limitations: For taxpayers with taxable income above the threshold, the deduction is subject to a limit that’s the greater of 50% of W-2 wages paid by the business or 25% of W-2 wages plus 2.5% of the unadjusted basis immediately after acquisition of all qualified property (tangible property subject to depreciation used in the business).

As the above points illustrate, the 20% pass-through deduction is complex and depends on various factors. It’s recommended that individuals consult with a tax professional to ensure they fully understand these rules and how they apply to their specific circumstances.

Image: Envato Elements

This article, “What Is the Qualified Business Income Deduction (QBI), and Can You Claim It?” was first published on Small Business Trends