Weight-management drugs known as GLP-1 receptor agonists have transformed the treatment landscape for both diabetes and obesity. However, their popularity has placed unprecedented financial strain on employer-sponsored health plans. Over the past year, the clinical and regulatory landscape of GLP-1s has evolved with new indications and approvals expanding their use.

Rising utilization and costs

The high cost is driven not only by the price of these drugs, but also by their expanded use for other conditions associated with cardiometabolic disease, such as obstructive sleep apnea. According to WTW’s 2024 Best Practices in Healthcare Survey, employers consider cardiometabolic disease a top health priority.

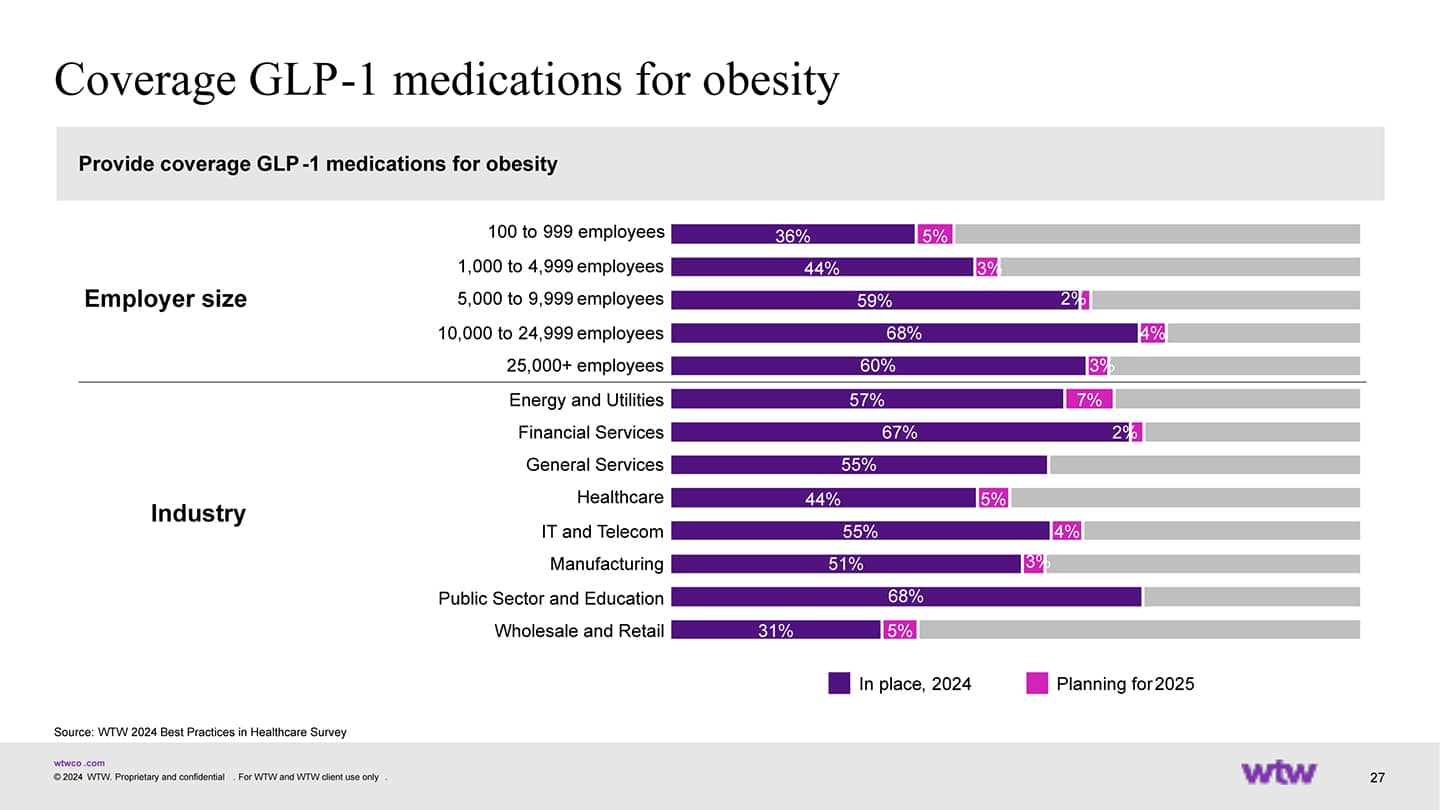

Of the respondents, 84% said diabetes was a top health priority, while 83% cited obesity and 56% said cardiometabolic disease. This focus aligns with the increase in utilization and pharmacy spend on these conditions.

See more: New anti-obesity drugs represent challenge, opportunity for employers

Despite the implementation of cost-containment strategies in recent years, GLP-1s continue to drive a substantial portion of the increase in pharmacy spending. More than half of employers (52%) in WTW’s survey reported they covered GLP-1s for weight loss. Seventy percent of those that did not cover GLP-1s for obesity said they might add coverage if the cost was lower.

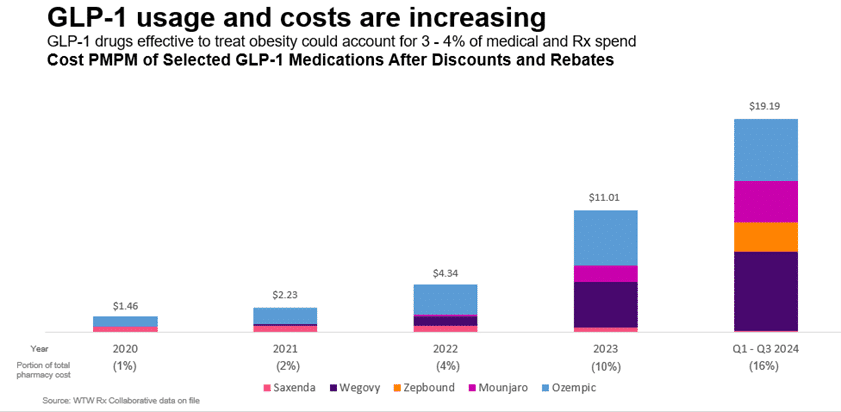

Cost per member per month (PMPM) increased exponentially from $4.34 in 2022 to $19.19 in Q1-Q3 2024.

Research shows that five GLP-1s account for 16% of the overall prescription cost for the Rx Collaborative, the largest pharmacy coalition in the U.S., after estimated rebates and discounts in Q1-Q3 of 2024, a rise from just 1% in 2020.

Key challenges with GLP-1s in 2025

Adherence issues and long-term use

Adherence to GLP-1s remains a significant challenge despite their proven efficacy in weight management and type 2 diabetes. While these drugs are designed for long-term use in disease management, many individuals use GLP-1s for a limited period—either to jump-start weight loss before transitioning to a lifestyle-based maintenance or due to financial constraints. A recent study indicated that patients with and without type 2 diabetes, 47% and 65% respectively, reported stopping the use of their GLP-1s within one year. However, 47% of those with diabetes and 36% with obesity who discontinued these medications restarted them again within a year.

Individuals with higher incomes and under age 55 were less likely to stop the medications, and those with obesity were more likely. This could be because those with obesity had a more difficult time obtaining insurance benefits for these expensive medications. Those who complained of gastrointestinal adverse effects were also more likely to discontinue use as well as those who lost more weight.

Multiple factors contribute to adherence, including discontinuation due to side effects, ineffectiveness, drug shortages, employer coverage and out-of-pocket costs.

Weight loss vendor landscape

Weight loss vendors are actively marketing to employers. According to WTW’s survey, 38% of employers have partnered with a third-party point solution vendor to support obesity management. For companies that cover GLP-1s for obesity, 14% required participation in a lifestyle modification program, 29% are planning this strategy for 2025 and 26% are considering for 2026.

Outcomes reporting has been limited from early adopters in these programs, with results difficult to interpret due to the fluctuating market. The net cost of the programs varies, and select PBMs are adjusting rebates and assessing integration and management fees when vendor programs are implemented.

In most cases, requiring members to enroll in a lifestyle modification program or limiting the prescribing of the drugs to certain specialists would result in a loss of rebates for GLP-1s for weight loss. Rebates are a valuable tool for negotiating price concessions from manufacturers when there are multiple competing products. However, most formularies cover both Wegovy and Zepbound, so rebates are currently not driving competition, but rather stifling innovative management strategies.

Vendors can differentiate themselves with meaningful performance guarantees and putting their fees at risk to ensure employers maintain the lowest net cost, inclusive of program fees and rebates.

With some employers not covering weight loss drugs, members are using direct to consumer (DTC) telehealth solutions to get brand and compounded drugs. There is ongoing litigation among manufacturers, compounding pharmacies and the FDA on how long compounding pharmacies can dispense the drugs, given that the FDA has announced the resolution of the shortage. The use of DTC pharmacies will continue to be high as long as access and cost are concerns.

Regulatory watch: Inflation Reduction Act and PBM pricing dynamics

Semaglutide (Ozempic, Wegovy, Rybelsus) was selected for Medicare price negotiation in 2025, which would take effect Jan. 1, 2027. The impact on commercial health plans is not yet known. In parallel, PBMs are facing increased scrutiny over their pricing practices and rebates. A recent Federal Trade Commission (FTC) report highlighted that leading PBMs have significantly inflated pharmacy costs, impacting both employers and employees.

For employers, these developments could lead to shifts in formulary decisions and cost-sharing strategies. The anticipated price reductions from Medicare negotiations may influence employer-sponsored health plans to adjust their coverage policies for GLP-1s. Additionally, the heightened scrutiny of PBM practices may result in renegotiated contract terms, potentially affecting employer cost burdens.

As of April 4, President Trump had rejected Biden’s proposal to expand GLP-1 coverage for obesity to Medicare and Medicaid. At this time, it’s unclear about the long-term ramifications of this decision.

Employers should stay informed about these regulatory changes to manage prescription drug costs and ensure employee medication access.

The next wave of GLP-1s: Pipeline and market expansion

Recent FDA approvals have expanded indications for cardiovascular risk reduction, sleep apnea and chronic kidney disease. Ongoing trials are investigating conditions, including Alzheimer’s disease, alcohol use disorder and metabolic dysfunction-associated steatohepatitis (MASH).

Researchers are studying alternate dosing schedules and higher doses. GLP-1s are also anecdotally being used in lower doses (“microdosing”); however, this has not been formally studied. Additionally, several next-generation GLP-1 therapies are in late-stage development, offering new administration methods and expanded indications in 2026.

What’s next for employers and GLP-1s?

Balancing access, cost and long-term outcomes

GLP-1s have revolutionized metabolic care, offering significant benefits for both diabetes management and weight loss. However, their financial sustainability remains an open question as utilization continues to rise, placing substantial strain on employer-sponsored health plans. With upcoming IRA price negotiations, potential PBM rebate structure reforms, and increasing regulatory scrutiny of DTC and compounded GLP-1 providers, employers must stay current with their formulary and coverage decisions.

According to WTW’s survey, employers that currently cover GLP-1 medications are also implementing restrictions. These include lifestyle modification requirements (69%), trialing lower-cost medications first (63%) and limiting therapy duration (63%). One in seven (14%) employers covering GLP-1s for obesity are considering discontinuation due to cost. Meanwhile, 20% report that they cover GLP-1s for obesity only at a BMI of 35 or more. Employers will have new opportunities to optimize their benefits as new GLP-1 formulations and competitors enter the market.

GLP-1 drugs offer members an expanding array of valuable clinical benefits but are very costly. Employers can stay ahead of the GLP-1 curve by proactively evaluating coverage strategies and vendors, monitoring utilization trends, and leveraging data-driven insights to manage costs effectively in 2025 and beyond.

The post The future of GLP-1 drugs for obesity treatment: cost, access and more appeared first on HR Executive.